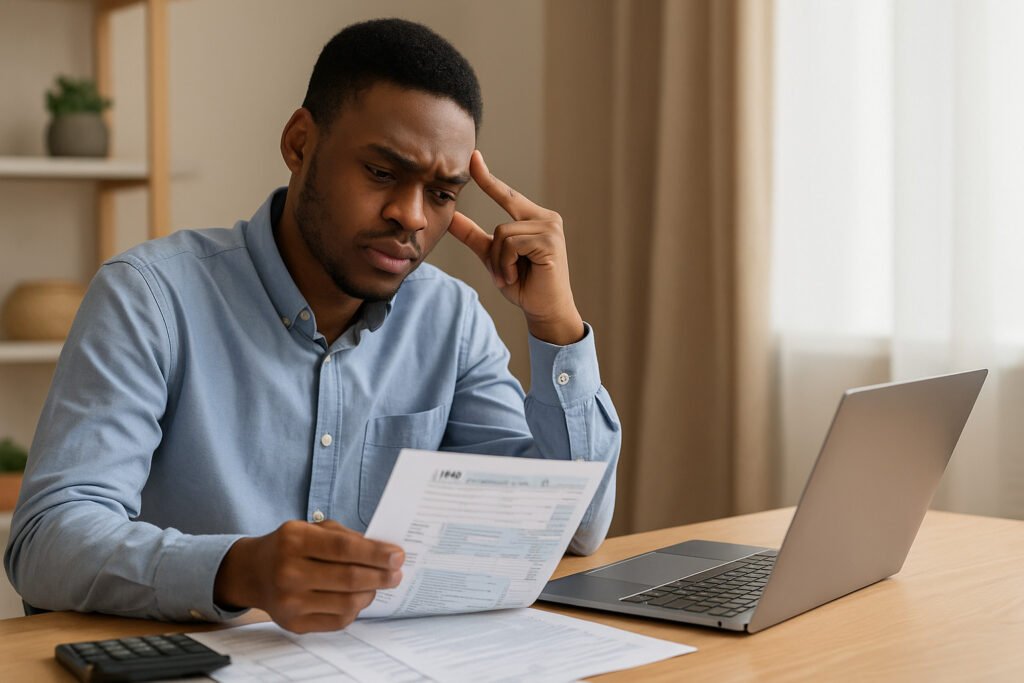

The Big Decision: LLC or Sole Proprietorship?

Starting or growing a business means making big choices, and one of the most important is your business structure. In 2025, entrepreneurs are weighing two popular options: LLC (Limited Liability Company) and sole proprietorship.

Why does this matter? Because your choice affects everything—from how you pay taxes to how easily you can get business loans. It also impacts personal liability, growth potential, and even credibility with lenders.

Choosing wisely gives you a solid foundation for expansion, whether you need small business loans for hiring, new equipment, or that dream commercial space. The decision can also influence your ability to access the best equipment financing and calculate real estate affordability with a commercial mortgage calculator.

Your business structure acts like the frame of a house. It supports everything else you build on top of it. A weak frame can limit your growth, while a strong one can support your ambitions for years to come.

What Exactly Is a Sole Proprietorship?

A sole proprietorship is the simplest business structure. It’s just you—no legal distinction between you and your business. Setting one up is easy, inexpensive, and perfect for freelancers or very small operations.

However, there’s a catch: You’re personally responsible for all debts and liabilities. If something goes wrong, your personal assets could be at risk. This can become a major concern if you plan to borrow or invest heavily in your operations.

For many, a sole proprietorship is a starting point. But as businesses grow, they often explore other options to protect their personal finances and qualify for better funding. Our blog on From Solo to Scalable: Smart Financing Paths for Sole Proprietors dives deeper into this transition.

Because a sole proprietorship is so simple, it’s attractive to first-time entrepreneurs. But that simplicity also means fewer protections. When applying for small business loans, lenders may see you as higher risk because there is no legal separation between you and the business.

What Is an LLC, and Why Is It So Popular?

An LLC offers more protection. It separates your personal assets from your business liabilities, making it a safer choice if you plan to take on debt or grow significantly.

LLCs also come with more credibility. Lenders often see them as more stable and professional, which can make it easier to secure small business loans or access the best equipment financing. Having an LLC attached to your name signals that you’re serious about running a legitimate operation.

While forming an LLC requires more paperwork and fees, the benefits—like limited liability and flexible taxation—are worth it for many entrepreneurs. You gain the confidence to invest in growth knowing your personal assets are safer.

Another benefit? LLCs are flexible in how they are taxed. You can elect to be taxed as a sole proprietorship, partnership, or corporation, depending on which option saves you the most money.

How Each Structure Affects Business Loans

Here’s where things get interesting. Lenders look at risk when deciding whether to approve you for financing. Because sole proprietors are personally liable, some lenders may hesitate to offer large business loans.

On the other hand, an LLC provides more security for the lender and borrower alike. You’ll often find more loan options, better terms, and higher approval odds as an LLC. Lenders see LLCs as a more structured and stable entity.

Whether you need small business loans for inventory or want to estimate payments using a commercial mortgage calculator, having the right business structure can make all the difference.

If you want to learn how to leverage depreciation to your advantage while seeking financing, check out our guide: Turning Depreciation Into Business Leverage. It highlights how certain financial strategies can improve your overall position when applying for loans.

Tax Differences You Shouldn’t Ignore

Taxes can be tricky, but understanding how each structure is taxed will save you headaches. Sole proprietors report income on their personal tax returns. It’s simple but can mean higher self-employment taxes.

LLCs have more flexibility. You can choose to be taxed as a sole proprietor, partnership, or even an S-corp. This flexibility can lead to significant savings, especially if you’re reinvesting profits back into the business.

Because taxes directly impact your take-home pay and ability to repay loans, understanding these differences is crucial. Better cash flow management can also help when you’re planning to invest in assets or apply for best equipment financing options.

Want to see how expenses like equipment depreciation can work in your favor? Our blog Turning Depreciation Into Business Leverage explains how to make smart financial moves.

Growth Potential: Which Structure Helps You Scale?

If you plan to stay small, a sole proprietorship might be fine. But if you dream of hiring employees, taking on investors, or expanding locations, an LLC is more appealing. Investors typically prefer more formal structures like LLCs or corporations because they seem more reliable.

LLCs are also more attractive to lenders and partners. When it’s time to apply for small business loans, credibility matters. And lenders are more likely to work with businesses that seem established and well-structured.

For more tips on managing growth and cash flow, check out our guide: Turning Cash Flow Chaos Into Control. It shows how to improve financial stability before taking on debt.

Growth potential also connects to your long-term goals. If you see your business expanding into multiple states or scaling operations, the structure of an LLC can provide the legal flexibility you’ll need for that growth.

Liability: Protecting Your Personal Assets

Liability protection might be the single biggest reason entrepreneurs choose an LLC. If your business gets sued or can’t pay its debts, your personal assets—like your home or car—are generally protected.

As a sole proprietor, there’s no separation. If something happens, your personal finances are on the line. This risk becomes especially important when borrowing larger amounts or entering into long-term leases.

Before signing agreements or using tools like a commercial mortgage calculator, think about the level of protection you need. Peace of mind can be worth the additional setup time and costs of forming an LLC.

Lenders also consider liability risk. Businesses with legal separation often receive better financing options because lenders know that structured entities can better manage financial obligations.

The Setup Process: Which Is Easier?

Sole proprietorships are quick to set up—often requiring just a business license. LLCs, while still straightforward, involve more steps like filing articles of organization and paying state fees.

However, that extra effort often pays off in better financing options and long-term growth potential. It’s a trade-off worth considering, especially if you plan to apply for business loans or best equipment financing in the future.

Additionally, LLCs allow you to create a more professional brand presence. Having “LLC” in your name can improve trust with customers, partners, and even investors.

So, Which Should You Choose in 2025?

There’s no one-size-fits-all answer. If you’re testing an idea or working solo with minimal risk, a sole proprietorship might be enough. But if you’re serious about scaling and want access to more funding, an LLC is the smarter move.

Consider your goals, risk tolerance, and growth plans. And remember, as your business evolves, you can always change your structure later. Many entrepreneurs start as sole proprietors but transition to LLCs as they expand.

For more insights on making financing decisions that fit your goals, revisit our blog on Turning Depreciation Into Business Leverage.

Choose With Your Future in Mind

Your business structure is more than a formality—it’s a foundation for success. It affects your taxes, liability, and even your ability to secure small business loans or calculate affordability with a commercial mortgage calculator.

Think about where you want your business to be in the next 5 years. Then choose the path that makes scaling, borrowing, and thriving easier.

Millendeal is here to guide you through every step of your financing journey. Whether it’s securing funding, upgrading equipment, or planning for expansion, we’re your partner in growth.

By thinking ahead, preparing your finances, and picking the right structure, you’ll set your business up for long-term success. Smart planning today leads to smoother borrowing tomorrow.